Rich Dad Poor Dad Summary & Infographic | Robert Kiyosaki

What The Rich Teach Their Kids About Money That the Poor and Middle Class Do Not!

Did you know 90% of millionaires build wealth through assets, not high salaries? Yet most people spend their lives working for money instead of having money work for them. What if everything you learned about money in school was designed to keep you financially struggling…?

Life gets busy. Has Rich Dad Poor Dad been gathering dust on your bookshelf? Instead, pick up the key ideas now.

We’re scratching the surface in this Rich Dad Poor Dad summary. If you don’t already have Robert Kiyosaki’s book, order it here or get the audiobook for free to learn the juicy details.

Disclaimer: This is an unofficial summary and analysis.

Rich Dad Poor Dad Summary | 10 Key Ideas & Quotes

| Element | Details |

| Book | Rich Dad Poor Dad by Robert T. Kiyosaki |

| Core Idea | Financial literacy and understanding the difference between an asset and a liability are the fundamental building blocks of wealth—not your salary or education. |

| Key Takeaways | 1. The rich don’t work for money; they have money work for them through assets. 2. Your primary residence is a liability, not an asset—focus on acquiring income-generating assets. 3. Financial education is your greatest asset and the key to escaping the “Rat Race.” |

| Best For | Anyone feeling trapped by their paycheck, seeking to break free from the “rat race,” and ready to build lasting financial independence through financial literacy. |

| Reading Time | 11 minutes |

Introduction

Ever felt like you’re on a hamster wheel, working harder but getting nowhere? That’s the “Rat Race,” says Robert Kiyosaki. It’s not about your income; it’s about your financial education. Rich Dad Poor Dad ignited a global movement by revealing a startling truth: the old advice of “school, job, save” is a trap. This Rich Dad Poor Dad summary shows you how the rich make money work for them, instead of the other way around. It has since become the #1 personal finance book of all time, transforming the way millions think about money and investing.

About Robert T. Kiyosaki

Robert T. Kiyosaki is an American businessman, investor, and author, best known for the Rich Dad Poor Dad series. A fourth-generation Japanese American and U.S. Marine Corps veteran, Kiyosaki founded the Rich Dad Company to provide financial education through books and seminars. His work has been translated into 51 languages and has sold over 41 million copies worldwide, making him one of the most influential voices in personal finance.

StoryShot #1: Why Do the Rich Not Work for Money?

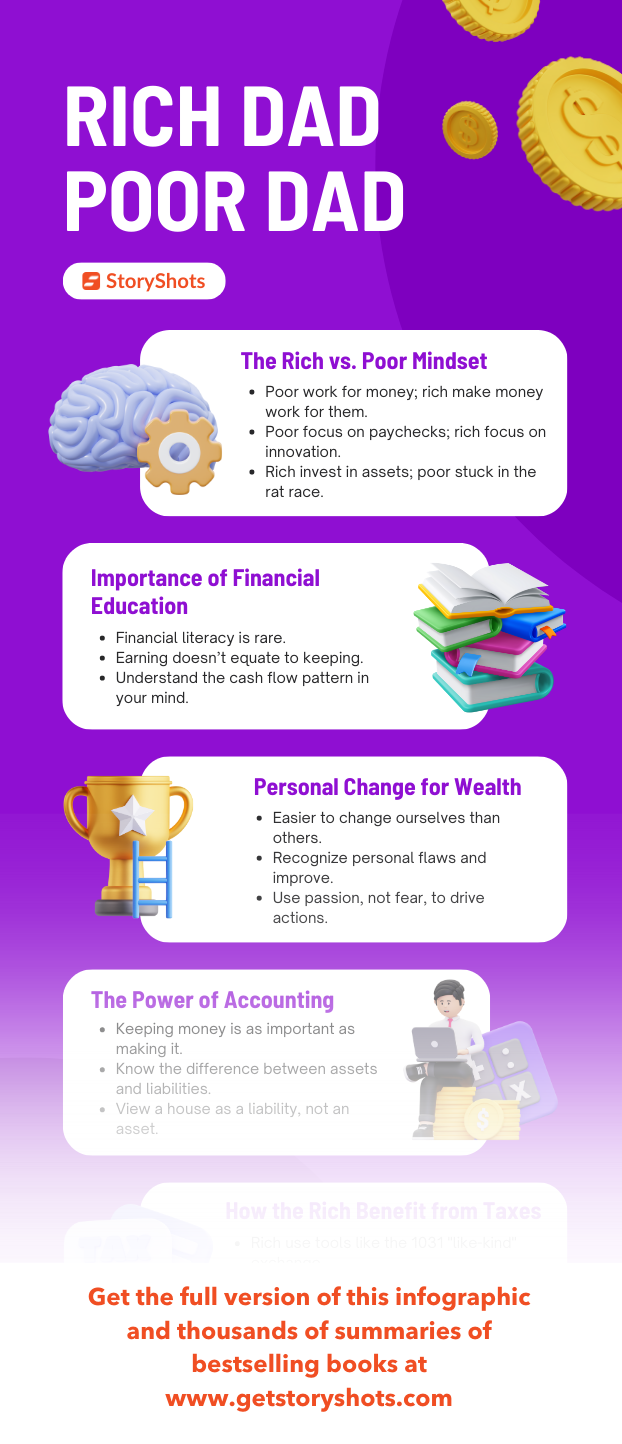

The typical career path—good job, steady paycheck—is a trap that leads to the “Rat Race.” Fear of poverty drives people to work harder, but more income just leads to more spending. You never get ahead. As Kiyosaki says, “Most people become a slave to money.” The rich, however, make money work for them. This isn’t about a job; it’s about becoming an investor. The goal is to acquire assets that generate passive income, freeing you from depending on a paycheck. It’s like planting a tree that provides fruit for years, instead of constantly chopping wood for a daily wage. That’s the secret to real wealth. This mindset shift is the first and most crucial step toward financial freedom.

StoryShot #2: What Is the Difference Between an Asset and a Liability?

Most people struggle financially because they don’t grasp the crucial difference between an asset and a liability. An asset puts money in your pocket. A liability takes money out. It’s that simple. The rich buy assets; the poor and middle class buy liabilities they think are assets. For example, a rental property generating positive cash flow is an asset. Your home’s mortgage, however, is a liability. Kiyosaki’s rich dad taught him, “Rich people acquire assets. The poor and middle class acquire liabilities that they think are assets.” This single distinction is the key to financial independence. Understanding this difference is the foundation of financial literacy.

Want to know the fastest way to build your asset column? Start small and focus on cash flow, not appreciation.

StoryShot #3: How Can You Mind Your Own Business?

Most people work for everyone but themselves: their employer, the government, and the bank. They focus on their profession, not their own business. Your profession is your job; your business is your wealth. To be financially free, you must mind your own business by focusing on your asset column. Keep your day job, but use your income to acquire passive income-generating assets. Your business is your asset column, not your salary. Real assets include businesses you don’t manage, stocks, bonds, and income-producing real estate. By minding your own business, you seize control of your financial future. This is how you build a foundation for lasting wealth.

Here’s the key: keep your day job, but make your real work building your asset column.

StoryShot #4: What Is the History of Taxes and the Power of Corporations?

Originally, only the rich were taxed. But the government’s appetite for money grew, and taxes were extended to everyone else. Today, the middle class bears the heaviest tax burden, while the rich use the tax code to their advantage. The wealthy use corporations to protect their assets and minimize taxes. A corporation is a legal entity separate from its owners, shielding personal assets from lawsuits. Corporations also offer huge tax advantages. Individuals are taxed before they spend; corporations are taxed on profits after expenses. This allows a corporation to legally write off a wide range of expenses, reducing its taxable income. This is a game the rich have mastered.

The difference? Employees earn, pay taxes, then spend. Business owners earn, spend, then pay taxes on what’s left.

StoryShot #5: How Do the Rich Invent Money?

As Kiyosaki states, “The single most powerful asset we all have is our mind. If it is trained well, it can create enormous wealth.” The rich know money isn’t real; it’s invented. This requires financial intelligence and seeing opportunities others miss. To invent money, develop your financial IQ by learning accounting, investing, and market dynamics. It’s about seeing what others don’t and taking calculated risks. As Kiyosaki writes, “Winners are not afraid of losing. But losers are. Failure is part of the process of success.” For instance, a financially savvy person might find a distressed property, buy it at a discount, renovate it, and then sell or rent it for a profit. They create value and, in essence, invent money. This is the ultimate form of financial creativity.

The question isn’t “Can I afford it?” but rather “How can I afford it?” That shift in thinking changes everything.

StoryShot #6: Why Should You Work to Learn, Not for Money?

Many chase high-paying jobs, thinking a bigger paycheck will solve their problems. This is a short-sighted view. The most valuable thing you can acquire in your career isn’t money, but skills. The rich work to learn, not for money. Instead of specializing, become a generalist, learning “to know a little about a lot.” This broadens your perspective and helps you spot opportunities specialists miss. The most vital skills are sales and marketing. You can have the best product, but if you can’t sell it, you won’t make money. By focusing on learning, you invest in your greatest asset: yourself. This is an investment with lifelong returns.

Don’t ask “How much will I earn?” Ask “What will I learn?” That’s the mindset of the wealthy.

StoryShot #7: What Are the Five Main Obstacles to Overcome?

Even with a solid financial education, many fail to achieve financial independence due to five obstacles: fear, cynicism, laziness, bad habits, and arrogance. Fear of losing money is the most common, paralyzing people from taking risks. Cynicism is another hurdle, as cynics always find reasons why things won’t work. Laziness, bad habits like overspending, and arrogance that prevents learning are also significant barriers. Kiyosaki stresses, “If you realize that you’re the problem, then you can change yourself, learn something and grow wiser.” Overcoming these five obstacles is essential for financial freedom. It’s an internal battle you must win.

The biggest obstacle to wealth isn’t lack of money—it’s lack of courage to face your fears.

StoryShot #8: What Are the Ten Steps to Get Started?

Getting started can seem daunting, but Kiyosaki offers ten steps. First, have a deep emotional reason to be rich. Second, choose to be rich daily through your spending. Third, choose your friends carefully. Fourth, master a formula, then learn a new one. Fifth, pay yourself first—a critical wealth-building habit. Sixth, pay your brokers well. Seventh, be an “Indian giver”—get your money back quickly on investments. Eighth, use assets to buy luxuries, not debt. Ninth, find a hero and learn from them. Finally, teach and you shall receive. These steps provide a clear roadmap to begin your journey.

Remember: action always beats perfection. Start small, but start today.

StoryShot #9: Why Is Financial Intelligence More Important Than Money?

In our changing world, financial intelligence is more important than ever. As Kiyosaki says, “I am concerned that too many people are focused too much on money and not on their greatest wealth, which is their education.” Financial intelligence is understanding and applying financial concepts—reading a financial statement, analyzing an investment, structuring a deal. It’s a learnable skill not taught in schools. Kiyosaki notes, “intelligence solves problems and produces money. Money without financial intelligence is money soon gone.” This is why lottery winners often go broke. By developing your financial intelligence, you invest in your most valuable asset: your mind. This is the ultimate form of wealth.

Think about it: would you rather have a million dollars or the knowledge to make a million dollars? The knowledge lasts forever.

StoryShot #10: What Is the Power of Giving?

Many think that to be rich, you must be greedy. The opposite is true. The most successful people are the most generous. They understand the power of giving and reciprocity. As Kiyosaki writes, “Whenever you feel ‘short’ or in ‘need’ of something, give what you want first and it will come back in buckets.” When you give, you signal to the universe that you have more than enough, creating a vacuum that attracts more abundance. It’s not about giving to receive, but from a place of genuine generosity. By embracing giving, you create a life of abundance and fulfillment. It’s not just about making money; it’s about making a difference. This is a spiritual law of wealth.

The paradox of wealth: the more you give, the more you receive. Try it and see for yourself.

Mental Models from Rich Dad Poor Dad

The Cashflow Quadrant

The Cashflow Quadrant divides people into four categories based on how they earn income: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). The left side (E and S) is where most people are, working for money with limited freedom. The right side (B and I) is where the rich are, having money work for them. True wealth comes from moving to the right side of the quadrant, where you create systems and assets that generate income without your direct involvement. This shift requires a change in mindset, skills, and income sources. It’s about moving from active to passive income. The goal is to move from the left to the right side of the quadrant.

Which side of the quadrant are you on? More importantly, which side do you want to be on?

Financial Independence Number

Financial independence is having enough passive income to cover your living expenses. It’s not about being rich; it’s about being free. To calculate your financial independence number, multiply your monthly expenses by 12 to get your annual expenses. Then divide that number by your expected annual return on investments (typically 4-8%, based on the 4% rule). The result is the amount of money you need in income-generating assets to be financially free. For example, if your annual expenses are $40,000 and you expect a 5% return, you need $800,000 in assets. That’s your target. This number makes your goal concrete and measurable. It transforms a vague dream into an achievable goal.

Implementation Guide

•Today (5 minutes): Calculate your net worth. List all your assets (things that put money in your pocket) and liabilities (things that take money out). Be brutally honest—your house is probably a liability. This is your financial starting line. This simple exercise will give you a powerful dose of reality.

•This Week (15 minutes): Read one chapter of a personal finance or investing book. Make it a habit to read at least one financial book per month. Knowledge is the new money. Start with The Intelligent Investor or The Simple Path to Wealth. You can also explore free financial education resources at Khan Academy. This small habit will pay huge dividends over time.

•Ongoing Practice: Track your expenses for 30 days. This will help you identify where your money is going and where you can cut back to redirect funds into acquiring assets. Use a simple spreadsheet or an app like Mint or YNAB. You can’t manage what you don’t measure. This is the first step to taking control of your money.

Final Summary

This Rich Dad Poor Dad summary has covered the essential lessons from one of the most influential personal finance books ever written. Rich Dad Poor Dad is a must-read for anyone who wants to achieve financial freedom. It challenges the conventional wisdom about money and provides a practical roadmap for building wealth. The book’s core message is that financial education is the key to a life of abundance. By learning the language of money and adopting the mindset of the rich, you can take control of your financial destiny and create a life of your dreams.

As Kiyosaki reminds us, “You’re only poor if you give up. The most important thing is that you did something.” Start today by calculating your net worth, reading a financial education book, and tracking your expenses. The journey to financial freedom begins with a single step. This book is not just about money; it’s about freedom.

The question isn’t whether you can afford to invest in your financial education. The question is: can you afford not to?

Related Book Summaries

•Rich Dad’s Cashflow Quadrant summary by Robert Kiyosaki — Ready to move from the left side of the quadrant to the right? Discover how Kiyosaki’s follow-up reveals the exact path from employee to investor, and why your income source matters more than your income amount…

•The Business of The 21st Century summary by Robert Kiyosaki — What if 72% of Americans would rather work for themselves but don’t know where to start? Discover why Kiyosaki believes network marketing is the ultimate path from the E and S quadrants to true financial freedom in the B quadrant, and how you can build a recession-proof business that works for you…

•Think and Grow Rich summary by Napoleon Hill — What if 13 principles could unlock unlimited wealth? Discover the timeless success philosophy that has created more millionaires than any other book, based on Hill’s 20-year study of the world’s richest people…

•The Intelligent Investor summary by Benjamin Graham — Want to learn the secrets of value investing that Warren Buffett used to build his fortune? Discover how Graham’s timeless principles can help you build a solid and profitable investment portfolio without gambling on hot stocks…

•I Will Teach You To Be Rich summary by Ramit Sethi — Ready to stop worrying about money and start living your rich life? Discover how Sethi’s 6-week program can help you automate your finances, eliminate guilt about spending, and build wealth effortlessly…

•How to Get Rich summary by Naval Ravikant — What if wealth isn’t about luck but about leverage? Learn how Naval’s unconventional wisdom on building wealth, happiness, and freedom can help you escape the 9-to-5 grind and create a life of abundance…

•Midas Touch summary by Robert Kiyosaki and Donald Trump — What do a real estate mogul and a financial educator have in common? Discover the five key entrepreneurial traits that Kiyosaki and Trump share, and how you can develop them to turn everything you touch into gold…

•Total Money Makeover summary by Dave Ramsey — Drowning in debt and living paycheck to paycheck? Discover Ramsey’s proven 7-step plan to eliminate debt, build an emergency fund, and achieve total financial peace, even if you’re starting from zero…

•Angel summary by Jason Calacanis — Ever wondered how early investors in Uber and Robinhood made millions? Learn the insider secrets of angel investing from Silicon Valley’s most successful investor, and how you can get started with as little as $1,000…

•The Millionaire Fastlane summary by M.J. DeMarco — Tired of the slow lane to wealth that takes 40 years? Discover how DeMarco’s Fastlane framework can help you build a business that generates massive wealth in years, not decades, and gives you the freedom to live life on your own terms…

Rating

We rate Rich Dad Poor Dad 4.3/5. How would you rate Rich Dad Poor Dad based on our summary?

Top Quotes from Rich Dad Poor Dad

“The poor and the middle class work for money. The rich have money work for them.”

“Rule #1: You must know the difference between an asset and a liability, and buy assets. If you want to be rich, this is all you need to know.”

“Winners are not afraid of losing. But losers are. Failure is part of the process of success. People who avoid failure also avoid success.”

“You’re only poor if you give up. The most important thing is that you did something. Most people only talk and dream of getting rich. You’ve done something.”

Infographic

Get the full version of this Rich Dad Poor Dad summary and infographic on the StoryShots app.

Rich Dad Poor Dad PDF, Free Audiobook and Animated Book Summary

This was the tip of the iceberg. To dive into the details and support Robert Kiyosaki, order Rich Dad Poor Dad or get the audiobook for free on Amazon.

Did you like the lessons you learned here? Comment below or share to show you care.

New to StoryShots? Get the PDF, free audio and animated versions of this analysis and summary of Rich Dad Poor Dad and hundreds of other bestselling nonfiction books in our free top-ranking app. It’s been featured by Apple, The Guardian, The UN, and Google as one of the world’s best reading and learning apps.

Too good.

My fav was work for the skill, not for the money. Totally resonates with me!

And generate assets that pay for your liabilities. Another super thought.

Thanks for sharing your thoughts!

Robert kiyosaki meu Mentor favorito

Thanks for your comment!

Thanks!

You’re welcome. Thanks for reading our content!

You’re most welcome. Thank you for your comment!